H&R Block: Insights on American Perseverance

Every year at H&R Block, we help millions of Americans with their taxes. This gives us a unique perspective on how people just like you are affected by significant events, including changes to tax policies.

We have a front row seat on the pulse of our country and how tax policy impacts consumers and business owners—both now and in the future.

We’re there for the good times, like that job promotion you deserved, buying your first house or even when you get married. We’re also there for the rough times, and it goes without saying, recently times have been rough.

However, we’re not here to talk about how this “new normal” has impacted the health, jobs, homes, and psyches of the American population.

What we want to talk about is how Americans, how you, rose above one of the weirdest times in U.S. history.

For most of you, it wasn’t simply about adapting to survive. You found a way to thrive.

Dreamers turned into doers. Savers got savvier. Families became stronger.

You showed us what you’re made of, and we want to show you what you accomplished. Our data on American life shows how you are changing the workforce, taking on the stock market, putting family first, and adapting through an incredibly difficult time.

Making Lemonade

You are breaking the mold of the modern workforce. What started as widespread unemployment has shifted into the Great Resignation. People everywhere are changing careers or exploring side hustles. Much of this was made possible by unemployment support delivered through the Coronavirus Aid, Relief, and Economic Security (CARES) Act, along with three rounds of federal stimulus payments.

Pre-pandemic, unemployment was typically higher among workers in the Northeast and Pacific West, while lower in the South. That pattern held during the pandemic. However, the amount of people claiming unemployment jumped 4 to 6 times across all income levels.

More women than men left the workforce, and roughly 40% of people who collected unemployment were women, compared with just 30% pre-pandemic. The less you earned, the more likely you were to be unemployed, and women earning between $10,000 and $30,000 annually reported nearly double the unemployment rate of men with the same income (25% vs. 14%).

Before the pandemic, job loss usually meant a dip in income. But with enhanced government unemployment support, most people making between $20,000 and $70,000 a year continued to report the same income even after losing their jobs.

Picture this: a single mother of two making around $28,000 a year. She’s already exhausted, having to balance full-time work with taking care of her children. Along comes the pandemic: a new level of crisis. She has few, if any, support systems in place when schools and daycares start to close. For her, staying home to care for her children is the only viable option. So, she leaves her job and collects unemployment. This gives her time not only to take care of her children, but eventually to look for a new job, possibly even a new career.

It’s simple to say that a spike in unemployment is a bad thing. However, you’ve shown us how to make the best out of a bad situation.

Hustling and Bustling

In response and out of necessity, a lot of you started new businesses or took on side hustles.

This makes sense when you think about it. At the beginning of the pandemic, everything was shut down. No concerts. Restaurants, bars and clubs all closed their doors. Even just hanging out was frowned upon. More people sitting at home with nothing to do. So, you thought of different ways to make money.

The CARES Act helped here, too, providing $1.9 trillion in grants, debt relief, and paycheck protection programs to help small businesses get back on their feet, supporting employee retention and offsetting lost or reduced wages. The Consolidated Appropriations Act of 2021 and the American Rescue Plan Act of 2021 extended or supplemented many of these provisions.

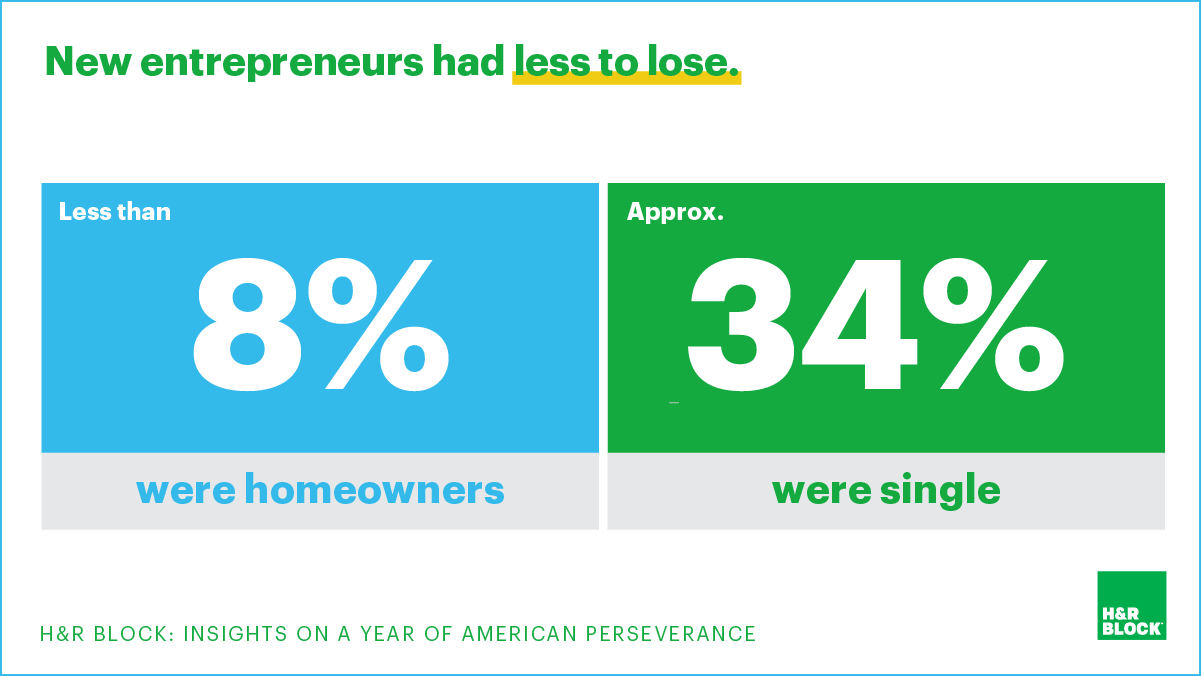

Nearly a quarter of new small businesses were started by people under 30, including 12% by 19- to 25-year-olds and another 12% by 26- to 30-year-olds. And these new entrepreneurs had less to lose. Less than 8% of new small business owners were homeowners, and about 34% of them were single. Plus, they were running lean, as only 14% made equipment purchases.

28-year-old Darell Dublin of Jersey City is a perfect example. For Dublin, the pandemic brought downtime. As soon as his day job transitioned to work from home, he had more time to invest in his fashion design business.

“I used the time to reevaluate my brand and decide on the direction,” says Dublin. “At the same time, I started making fabric masks in late March.”

By August, Dublin took up a gig with Shipt. He became a personal shopper for goods ranging from home décor to clothing and groceries.

But it isn’t just young Americans like Dublin who started new businesses. The average age of new entrepreneurs was nearly 42 years old, and nearly half were parents.

Back in June 2020, Ron Smith opened GiGi’s Bait and Tackle in Olathe, Kan. As an avid fisherman, Smith knew the closest bait shops in his area were 30 minutes away. He saw an opportunity for his new family business, despite the pandemic.

“God put it on me,” says Smith. “I just woke up one morning and we had been stuck in the house for [coronavirus] and…the bait shop came to my head.”

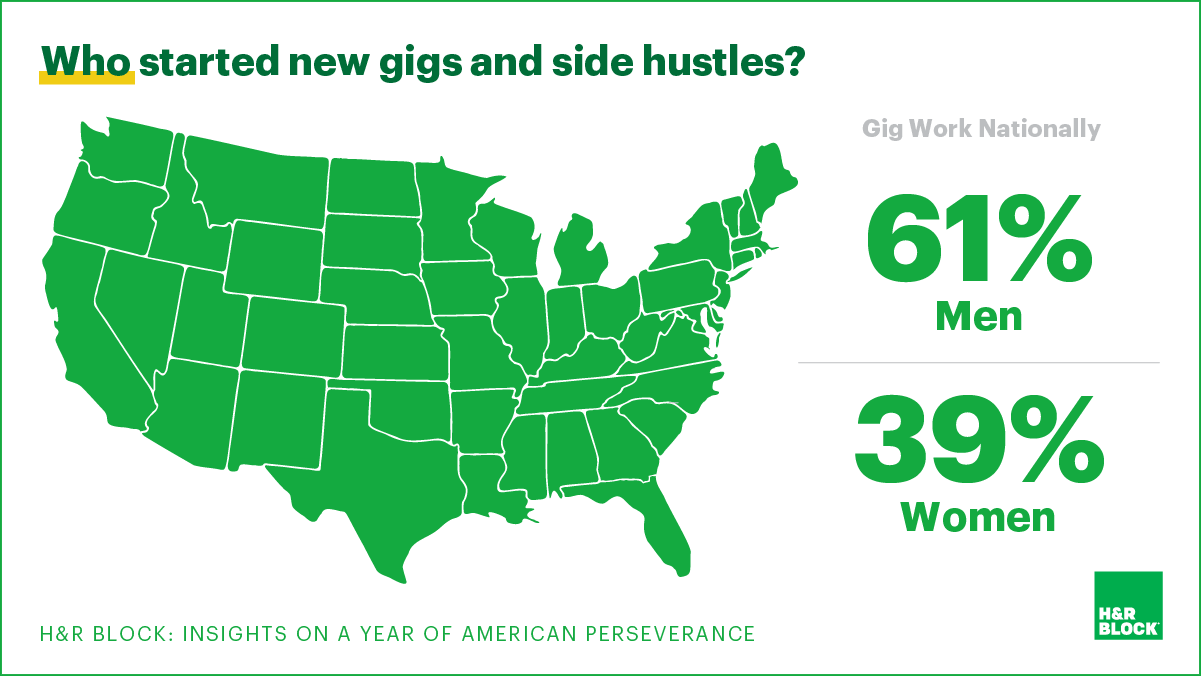

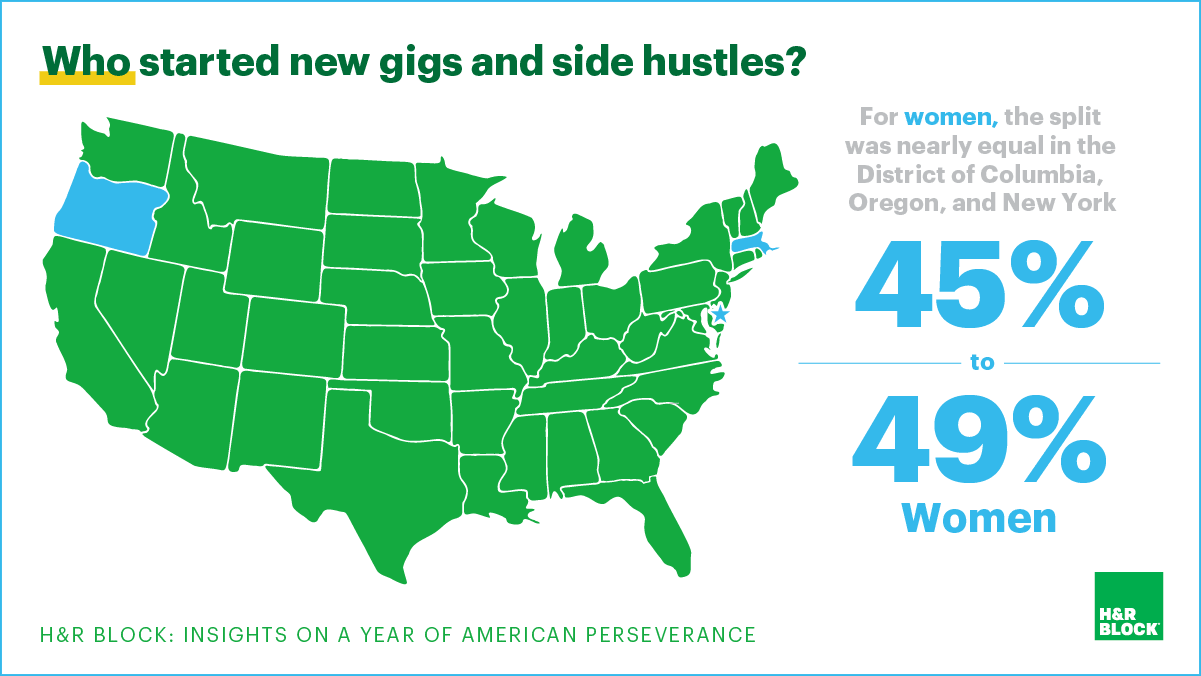

We didn’t just see a spike in new small businesses. A lot of you took up gig work and side hustles, with the highest concentration being men in Colorado, Georgia, and Idaho.

According to H&R Block Tax Pro Shirley Dooley, a big source of gig income was in delivery services, everything from groceries to meals.

“People that were laid off or who had less hours at work started delivering for companies and were able to quickly join places like DoorDash or Amazon,” says Dooley, “They were able to deduct expenses like mileage, but they also were learning about income as a contractor and not an employee for the first time.”

These additional wages helped offset reductions in primary income, and helped many people to set up many small businesses for the first time.

Going Back To Class — Investing 101

You’re also getting smarter with money. A lot smarter.

More people, especially young people, have begun participating in the stock market—and making money. This started with the rise in retail trading platforms, which provided a new way to get into the markets and began to democratize investing.

20- to 30-year-olds saw a staggering average growth of 70% in investing income for the first time, and even those under the age of 20 saw an average growth of 31%. So maybe youth isn’t always wasted on the young.

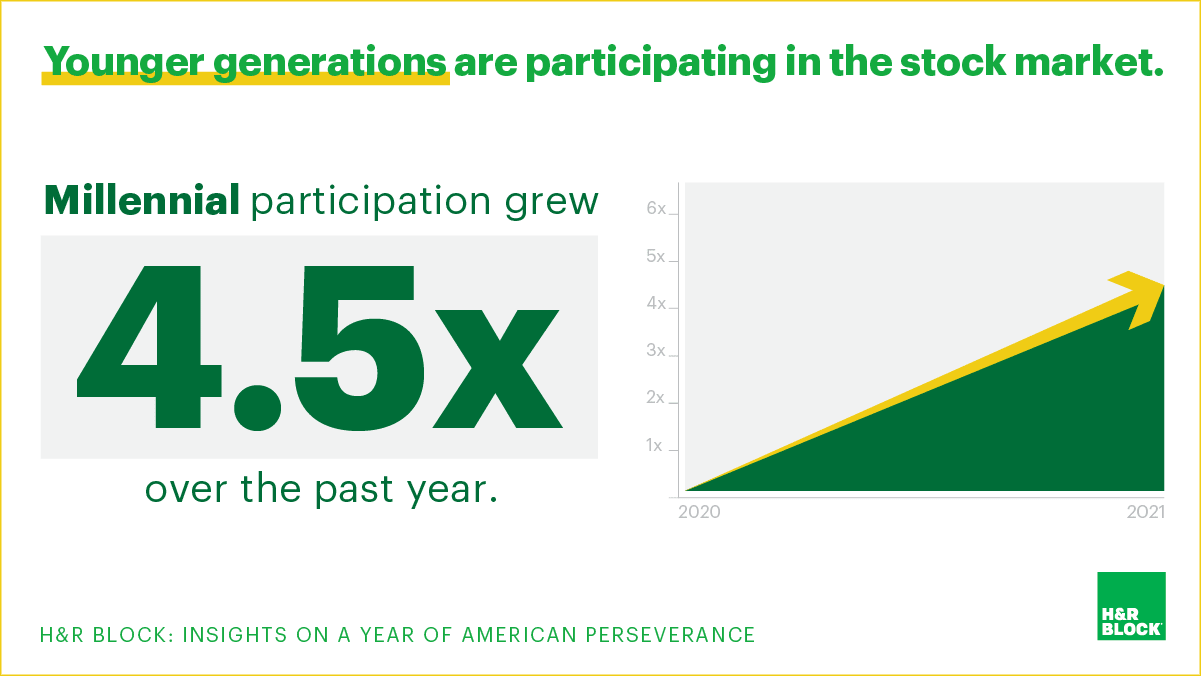

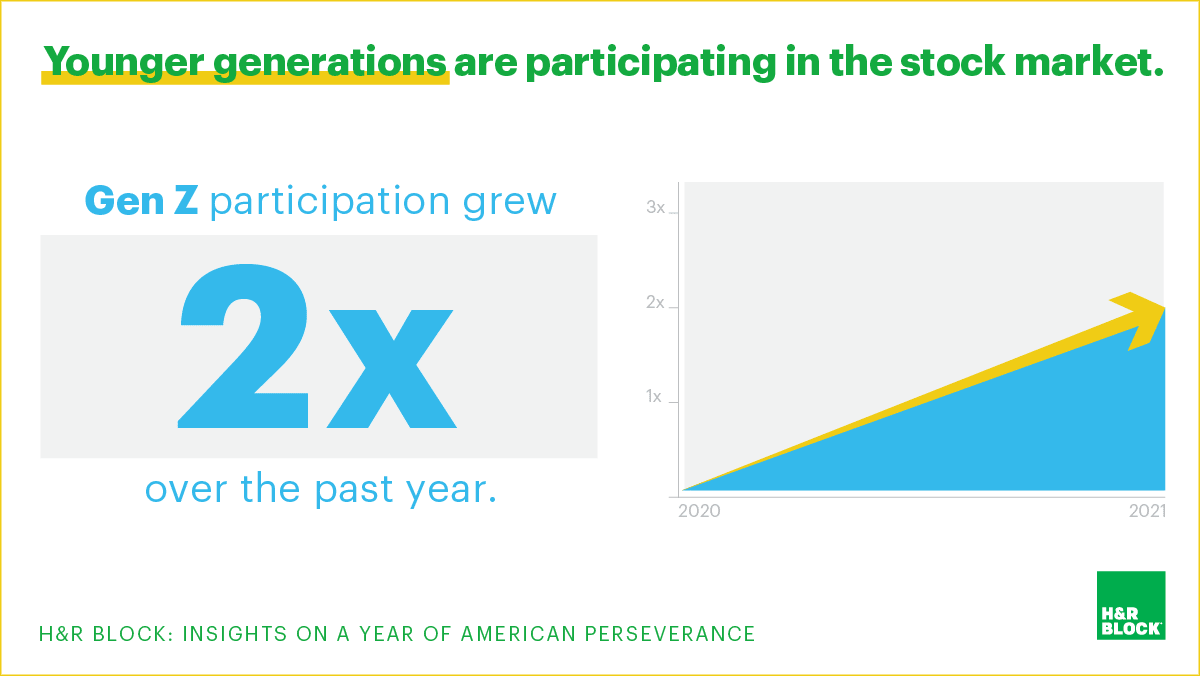

Millennials, especially, are making a splash in the stock market. Their participation grew 4.5 times over the past year. Gen Zers are also investing in the market, with their participation growing 2 times over the past year.

The frenzy in the stock market was real. And so was the effort to monetize other kinds of less-liquid assets. People making money from selling stock, land or businesses was 31% higher than 2019, 19% higher than 2018, and 42% higher than 2017.

Cryptomania

But what about cryptocurrency?

According to our data, young people under 29 made money in cryptocurrency last year—55% more than older generations. Gen Zers and Millennials alike saw a 155% year-over-year increase in crypto-linked profits.

What’s more, 76% of single tax filers who made money in crypto last year were men. In comparison, the ratio of men to women among single filers for all income is 49% to 51%.

So why is it that more young men are suddenly trading in cryptocurrency? They don’t exactly fit the profile of a traditional stock market investor. Our theory is that millennials are more comfortable with technology, and may be less trustworthy of the centralized banking system. Born in the early 1980s, millennials grew up in a world that frequently had some sort of financial crisis, from Black Monday in 1987, to the housing bubble burst in 2007. What’s more, millennials were also the first generation to grow up with modern personal computers and the Internet.

Crypto appears here to stay and it will be interesting to see how tax and other policies will adapt to its increasing popularity.

Retirement Remained Untouched

We also saw fewer Americans pulling from their retirement savings to get by during the pandemic, despite an increased ability to do so given new flexibility on certain government rules around early withdrawals.

In previous years, Americans on unemployment were 2.6 times more likely to tap into retirement savings than those not on unemployment. Over the last two years, Americans on unemployment were only 1.8 times more likely to tap into their retirement savings early, keeping those incredibly important nest eggs intact.

In a few places, though, there was still a need to tap retirement savings at a higher rate. Utah, Virginia, and Vermont had the highest rates of early withdrawals, with Utah residents withdrawing early at a 63% higher rate. In comparison, Washington, D.C.’s early withdrawal rate was 38% below the average.

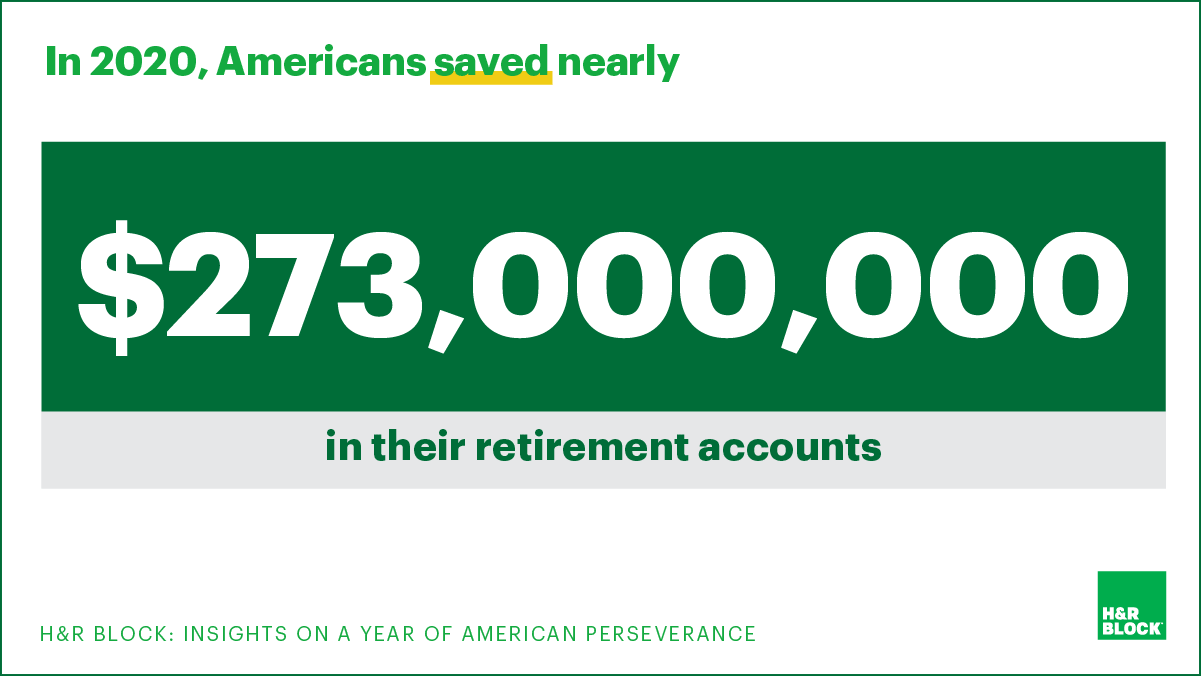

To put this all into perspective, Americans overall saved an estimated $273 million in retirement accounts, in just the last year alone. With interest accrual, that translates to a potential for a collective billion dollars over their lifetimes.

Family Ties

We don’t need to tell you that family life is changing. Children are attending Zoom meetings. Dogs are getting more walks than they could ever dream of, and cats despise you for being home all day. And, you probably had to cancel holiday plans and get creative with birthdays.

But from our vantage point, you also started a new family lifestyle.

There was a 13% increase in teenagers and 20-somethings filing taxes for the first time, instead of their parents claiming them as dependents. Why? Because these newbies could take advantage of stimulus payments and get as much as $3,200. Smart move.

Speaking of moves, some of you moved the whole nest. We all love fantasy house hunting, apartment therapy tours, or daydreaming of buying a tiny house. But historically, only 3% of people move year over year. What we found interesting is that a lot of folks that did move, perhaps spurred by the pandemic, chose to move to new types of neighborhoods.

Statistically, people tend to stay within the same type of neighborhood when they move. So, if you are a suburbanite, you stay in the suburbs, and same for those living in urban areas. However, starting in 2020, we saw that more than 44% of people moving into urban areas were from other types of neighborhoods, such as rural areas and suburbs. Mostly, these are families with $100,000 or more in annual income, and they were concentrated in Arizona, California, Connecticut, Massachusetts, New Jersey and Washington.

Then there were the couples under 40, with no children and making more than $100,000. They were the biggest movers, with Southerners moving to the mountains in the West, Northeasterners moving to the South, and Pacific Westerners moving to Texas, Oklahoma, Arkansas and Louisiana.

So who didn’t move? A couple making less than $50,000, with parents over 50, were more likely to stay in the same zip code – 93% compared to the national average of 86%.

Spending Habits Changed

This one’s a given, but still worth talking about. We all know that being stuck at home for a year made for some interesting purchases for Americans. However, our data shows that spending was geared more toward necessities than “nice to haves”. Americans were more likely to buy a new air filter for their AC than a new flat screen TV.

You probably saw this coming, but Amazon purchases increased 82% in 2020 for H&R Block Emerald Card account holders, as did food delivery purchases. For those who don’t know, our Emerald Card is a reloadable prepaid debit card for direct deposit of your tax refunds, but can be reloaded to make purchases and pay bills.

For Health Educator Reagan Tuff in Atlanta, GA, shopping was completely redefined.

“I started using Instacart and getting grocery deliveries immediately when we began working from home,” says Tuff. “I also stopped spending money on eating out or grabbing fast food since I was always at home.”

For Tuff, going out to shop was no longer a form of socializing or entertainment. Instead, it was done at home.

“I am spending a lot less money shopping,” says Tuff. “I’m really just focused on things I need.”

And with everyone sheltering in place, people started a lot more projects around the house. According to H&R Block Tax Pro Shirley Dooley, small business clients in the home improvement business, as well as car mechanics, had a busy 2020.

“People were in their homes more than ever and they were looking for contractors to make improvements and make the home more comfortable. Those businesses definitely saw an increase in demand and the matching revenue,” says Dooley.

People were also focused on keeping their used cars running, rather than buying new ones. “Mechanics were busy, and people were spending more on auto repair than they might have pre-pandemic because they wanted to avoid buying a new car,” says Dooley.

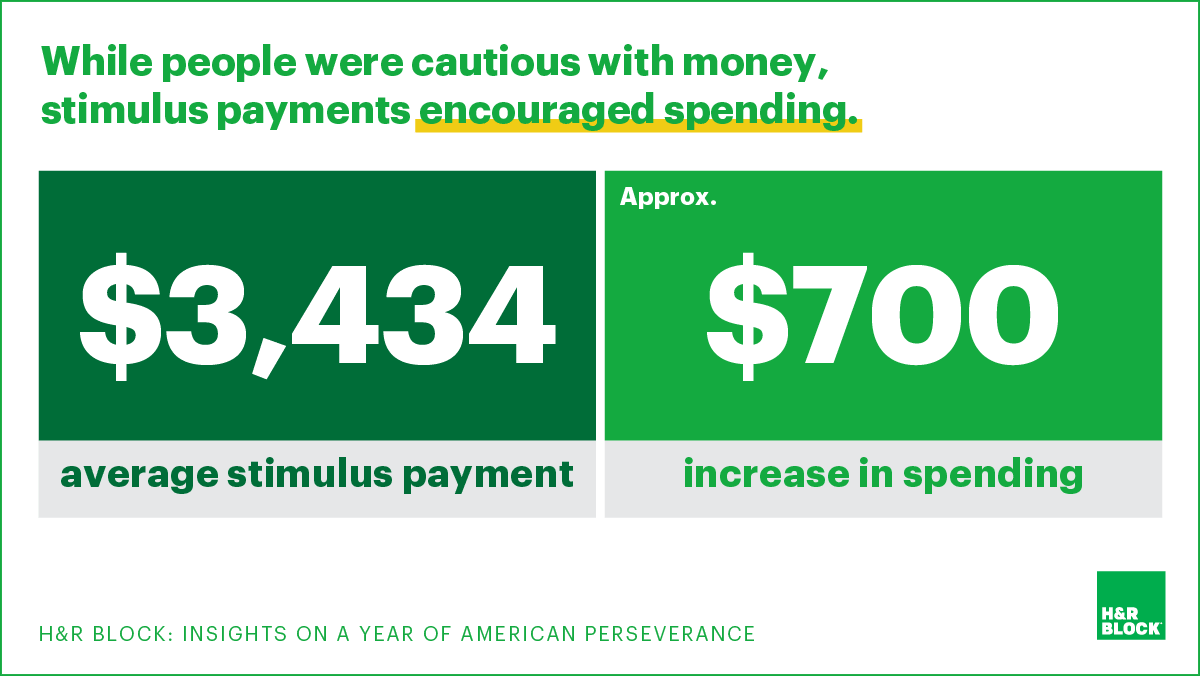

As thrifty as most of you were, we did notice that the Economic Impact Payments (a fancy way of saying “stimulus checks”) did encourage some spending. The average stimulus payment was $3,434. For those who received stimulus payments, we saw spending increase by about $700 in the months following those payments. Fun fact: about 5% of H&R Block Emerald Card clients did spend some of their stimulus on fast food.

In short, most Americans became more conscious spenders. You might have become a bit thriftier, but despite the new normal, no one can deny the occasional craving for a double cheeseburger with fries.

What’s Next?

So, what does the future look like?

Overall, the unprecedented fiscal stimulus programs enacted due to the pandemic provided Americans with vital financial support during difficult times. The impact of the pandemic—and the tax policies enacted in response—will be studied for years to come. Insights from our data provide some real-world examples around how tax policies can influence behaviors, in both expected and unexpected ways. In fact, many changes are already evident.

Studies show that over 50% of Americans are still looking to change jobs this year. There is a whole new generation of independents who have joined a rapidly changing workforce. Where people choose to live is impacted by the potential to work remotely. On top of that, the birth rate has dropped, and people are still making money in the stock market and cryptocurrency.

With all the shifting dynamics of daily life in America, it’s hard to say exactly what the future looks like and how future changes to tax policy may affect how it takes shape. It’s even harder to say what your future looks like. When it comes to seeing what’s on the horizon, rest assured: H&R Block has your back, and is here to help you navigate through all these uncertainties.

Was this topic helpful?