Questionable education credits draw IRS interest

The bottom line: IRS finds a way to question education credits

Two education tax credits, the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit (LLC), help taxpayers get back some of the costs of higher education through their tax returns.

Congress put both credits in place in 1997, and renamed and expanded the AOTC in 2009 to allow up to $1,000 of the credit to be refundable. With refundable credits, taxpayers get any extra credit back as a payment after all their taxes have been paid.

In 2015, almost 13 million taxpayers claimed the AOTC or the LLC on their 2014 tax returns. However, where there is complexity and the potential for financial gain, there are often errors and abuse. In 2015, the Treasury Inspector General for Tax Administration (TIGTA) found that more than 3.6 million taxpayers potentially received erroneous education credits. The IRS validated TIGTA’s suspicions when the IRS conducted audits of taxpayers with education credits.

Requirements for the AOTC and LLC can be complex

Education credits can be somewhat confusing. For either the AOTC or LLC, a taxpayer must meet these three conditions:

- The eligible student must be enrolled at an eligible educational institution,

- The eligible student is the taxpayer, the taxpayer’s spouse or the taxpayer’s dependent listed on the tax return and

- The eligible student’s qualified higher education expenses were paid by the taxpayer or the taxpayer’s dependent, relatives or friends.

However, the partially refundable AOTC has additional stringent qualifications compared with the LLC:

- Time limit: AOTC is allowed for four years of post-secondary education, whereas LLC has no limit on years.

- Degree-seeking requirement: AOTC requires that the student pursue a degree or other recognized education credential. The LLC doesn’t have this requirement and can be used for courses to acquire or improve job skills.

- Enrollment requirement: AOTC requires the student to be enrolled at least half-time. The LLC requires as little as one class.

- Drug conviction prohibition: People with a felony drug conviction can’t get the AOTC. LLC doesn’t have this limitation.

The IRS looks for the Form 1098-T true-up

TIGTA’s past concerns with taxpayers who take the AOTC focused on taxpayers who were taking the credit but didn’t receive Form 1098-T, Tuition Statement, from their educational institutions. The form reports payments received and/or billed for qualified education expenses. The IRS considers this information statement critical for claiming the credit because the form provides assurance from the eligible educational institution that the taxpayer paid qualified expenses during the year. Without this information statement, per TIGTA’s concerns, there’s no way to know whether the students were paying expenses or attending a qualified educational institution.

The IRS hasn’t always been able to comprehensively track the Form 1098-T. But because of new rules coming into effect for 2017 tax returns, the IRS will have improved visibility to the amounts that eligible institutions bill and receive as payment for students claiming the AOTC. When fully implemented, these new rules will require educational institutions to issue Forms 1098-T to all eligible students and to report the amount of qualified education expenses that were paid as opposed to reporting amounts billed. These two new requirements will provide the IRS with the information it needs to question the accuracy of education credits.

Along with these changes, the IRS will continue to streamline its questioning of tax returns claiming education credits using automated information matching.

IRS using automated matching to question more returns with education credits

Information statements (such as Forms W-2, 1099, 1098-T, etc.) are one of the most effective tools the IRS uses to detect and correct noncompliance. Through its Automated Underreporter (AUR) program, the IRS matches the 2.9 billion information statements filed each year to the 152 million individual tax returns filed. If there’s a mismatch, the IRS sends a notice (called a CP2000 or underreporter notice) to ask the taxpayer to correct the return. Underreporter notices are not audits, but they feel a lot like an audit to taxpayers.

In 2015, the IRS detected more than 27 million returns with a mismatch discrepancy. Last year, the IRS sent 3.5 million CP2000 notices to taxpayers questioning the accuracy of their returns. In comparison, last year, the IRS could audit only 1.3 million tax returns – far less than it achieved through the automated and streamlined AUR program.

In the past, the IRS relied on audits to question education credits. However, in the past two years, the IRS has used the AUR and CP2000 notices to question more of these returns.

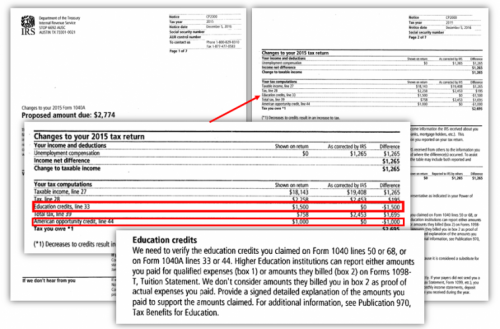

For example, here is a common CP2000 notice seen during the past two years. When the eligible education institution completes the Form 1098-T with only the amounts billed (box 2) and not the amounts paid (box 1), the IRS asks the taxpayer to verify that he or she has paid the expenses (and not just incurred them).

The CP2000 provides an adjusted tax calculation if the taxpayer can’t prove that he or she paid the expenses. Taxpayers often confuse the adjustment and additional tax proposal as a final ruling by the IRS, but it’s just a proposal at the CP2000 stage. Taxpayers should send the IRS proof that they paid the expenses. (see IRS Publication 970 for more information on what constitutes proof).

The bottom line

Based on studies, the IRS believes that many education credits are taken erroneously. The IRS is especially concerned with the AOTC, because up to $1,000 of it can be refunded to the taxpayer.

To combat noncompliance, the IRS is using its automated-matching program and Form 1098-T to check the accuracy of returns with education credits. Taxpayers should take care and closely review the complex rules in qualifying for education credits. Taxpayers also shouldn’t rely solely on Form 1098-T; they should make sure they have paid the expense before taking the credit.

If questioned by the IRS, taxpayers can be prepared with records that show the student was enrolled and the amount of paid qualified tuition and related expenses. If all of this sounds confusing, it’s because the rules for education credits are complicated.

Qualifying for tax credits can be confusing, so it’s best to see a tax pro for a tax prep appointment – and avoid the hassles of IRS notices.

Was this topic helpful?